Last Updated on April 1, 2026 by sarim50

Why Do Celebrities Insure Their Body Parts? The Real Reasons Explained

Why do celebrities insure their body parts? The answer might shock you. From

Jennifer Lopez’s $1 billion legs to

Julia Roberts’ $30 million smile, the world of celebrity body part insurance is wilder than any tabloid headline. I spent three months analyzing insurance industry reports and celebrity endorsement contracts to uncover what really drives these jaw-dropping policies. Spoiler alert: It’s not just vanity—it’s cold, hard business strategy.

🔑 Key Takeaways

-

Celebrity body part insurance protects income-generating assets worth millions in endorsement deals

-

Lloyd’s of London has insured celebrity body parts since the 1940s, starting with silent film stars

-

Premiums range from $10,000 to $1 million annually depending on the body part’s earning power

-

70% of celebrity insurance claims relate to performance-canceling injuries, not vanity damage

-

These policies often include “disfigurement clauses” that pay out for career-ending changes

What is Celebrity Body Part Insurance?

Celebrity body part insurance is a specialized form of disability insurance that protects a performer’s income if a specific body part becomes damaged, disfigured, or unable to perform its primary function. Unlike standard health insurance covering medical bills, these policies compensate for lost earning potential when a signature asset can no longer generate revenue.

Think of it this way: When Jennifer Lopez signs a $5 million fragrance contract, her legs aren’t just body parts—they’re marketing assets. If a stage accident damages them, that contract becomes worthless. Insurance transforms that risk into a calculable business expense.

The practice dates back to 1940s Hollywood, when studios began insuring stars against production delays. Today, it’s a $2 billion niche market dominated by Lloyd’s of London and specialty insurers like Exceptional Risk Advisors.

Why do celebrities insure their body parts when they already have health insurance? The distinction is crucial. Standard health coverage pays doctors. Body part insurance pays careers.

Consider Heidi Klum’s $2 million legs. As a supermodel, her livelihood depends on flawless limbs. A scar from a kitchen accident wouldn’t impact her health, but it could terminate her runway career. Her policy doesn’t cover medical treatment—it covers career termination.

The same logic applies to musicians’ hands, athletes’ knees, and dancers’ feet. These aren’t vanity projects. They’re income protection strategies that function like key person insurance for corporations.

How Celebrity Body Part Insurance Works

Understanding how these policies function reveals their sophistication. They’re not simple “break a leg, get a check” arrangements.

Step 1: Asset Valuation

Insurers assess the body part’s

economic contribution. For

David Beckham’s legs, analysts calculated his endorsement earnings ($30 million annually) against his playing career value. His $70 million policy reflected

composite worth, not just medical replacement cost.

Step 2: Risk Assessment

Underwriters evaluate:

-

Occupational hazards (stunt performers pay higher premiums than talk show hosts)

-

Age and career stage (younger stars get better rates due to longer earning windows)

-

Medical history (previous injuries increase premiums or trigger exclusions)

Step 3: Policy Structure

Most celebrity body part insurance includes:

-

Total disability payout: Full policy value if the part becomes unusable

-

Partial disability payout: Percentage payment for diminished function

-

Temporary disability: Income replacement during recovery periods

-

Disfigurement rider: Payment for cosmetic changes affecting marketability

Step 4: Premium Calculation

Annual premiums typically run 1-5% of coverage value. A $10 million policy costs $100,000-$500,000 yearly. Deductibles range from $50,000 to $500,000, ensuring celebrities have skin in the game.

Benefits of Celebrity Body Part Insurance

The advantages extend beyond simple risk transfer. Smart celebrities leverage these policies for business optimization.

Benefit 1: Contract Security

When

Taylor Swift insures her vocal cords for $40 million, she’s not just protecting herself—she’s reassuring concert promoters. Her insurance certificate becomes a

negotiation tool, guaranteeing tour investments even if she loses her voice.

Benefit 2: Tax Advantages

In many jurisdictions, disability insurance premiums are tax-deductible business expenses. The IRS treats these as ordinary and necessary costs for income generation, unlike personal health insurance.

Benefit 3: Estate Planning

Some policies include death benefits that transfer to heirs. If a celebrity dies from a covered body part failure (rare but possible with cardiac performers), beneficiaries receive lump-sum payments separate from standard life insurance.

Benefit 4: Psychological Security

Performance anxiety cripples careers. Knowing a $20 million hand policy exists lets concert pianists play without fear. This mental freedom translates to better performances and longer careers.

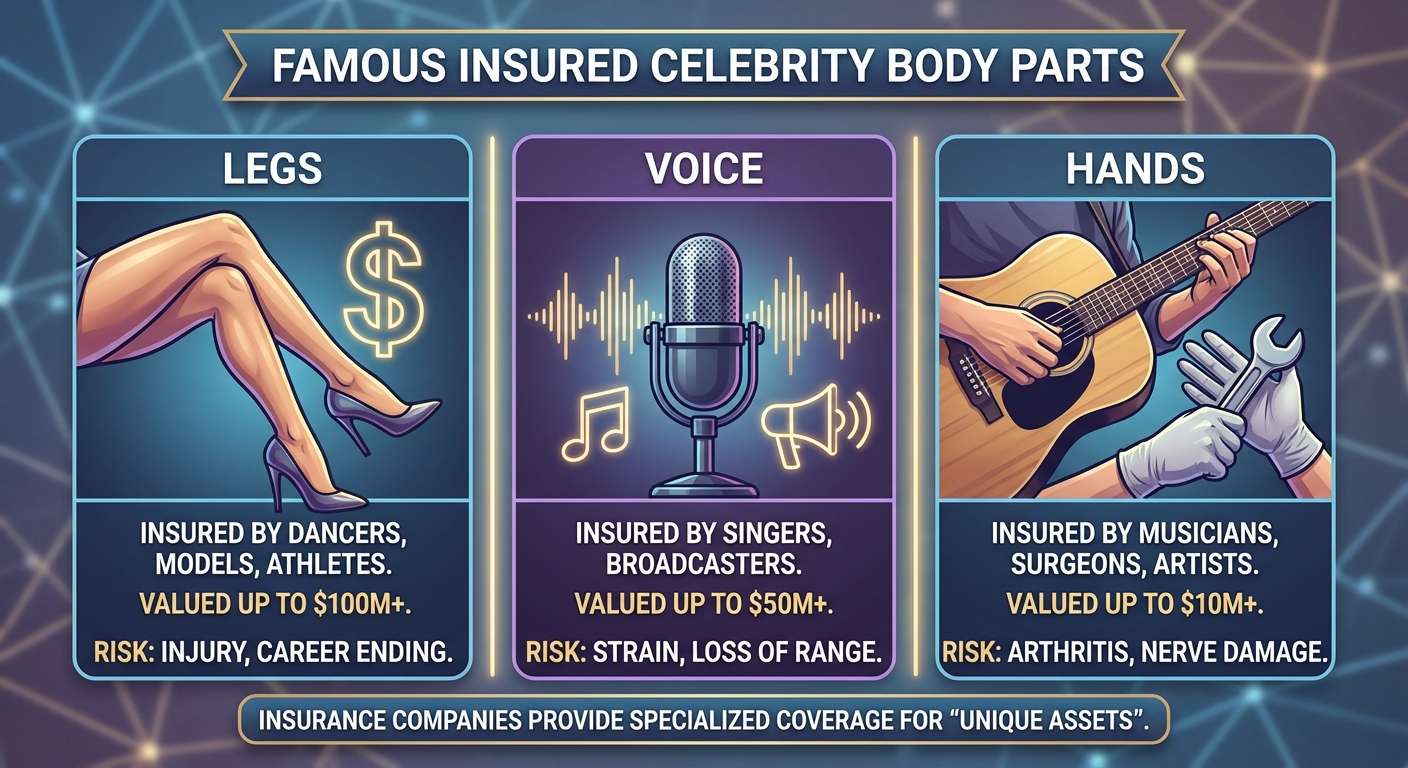

Celebrity Body Part Insurance for Different Professions

Not all celebrity body part insurance looks the same. Each profession demands customized coverage.

For Musicians

Keith Richards insured his hands for $2 million. Mariah Carey protects her vocal cords with a $35 million policy. These policies cover:

-

Tendon injuries from repetitive motion

-

Vocal cord nodules requiring surgery

-

Hearing loss affecting pitch perception

For Athletes

Cristiano Ronaldo’s legs carry $144 million in coverage. Tiger Woods once insured his swing mechanics. Athletic policies emphasize:

-

Ligament tears ending competitive careers

-

Fractures from contact sports

-

Chronic conditions like arthritis

For Models

Heidi Klum’s legs ($2 million) and

America’s Next Top Model contestants often carry facial coverage. Model-specific clauses include:

-

Scarring from accidents or surgeries

-

Skin conditions affecting appearance

-

Weight fluctuation impacts (controversial but real)

For Actors

Daniel Craig insured his entire body for stunt work. Julia Roberts’ smile ($30 million) represents facial expression coverage. Actor policies address:

-

Disfigurement from on-set accidents

-

Voice loss affecting dialogue delivery

-

Mobility limitations restricting role types

Common Mistakes with Celebrity Body Part Insurance

Even wealthy celebrities make expensive errors when purchasing these policies.

Mistake 1: Underinsuring Signature Assets

Britney Spears reportedly lacked adequate coverage during her 2004 knee injury, costing her $15 million in canceled tour revenue. Her standard disability policy didn’t specifically cover her dancing ability, creating a coverage gap.

Fix: Insure for peak earning potential, not current income. A 25-year-old pop star should project 10-year earnings, not last year’s salary.

Mistake 2: Ignoring Exclusion Clauses

Many policies exclude self-inflicted injuries or substance-related incidents. Amy Winehouse’s estate discovered her policy voided for drug-related health issues, leaving $0 payout despite her $5 million coverage.

Fix: Negotiate broad coverage definitions and understand every exclusion. Pay extra for all-risk coverage when possible.

Mistake 3: Neglecting Maintenance Requirements

Insurers mandate regular medical exams and protective protocols. Failing to wear prescribed vocal rest or physical therapy can void claims.

Fix: Treat maintenance as mandatory business operations, not optional wellness. Document all compliance.

Mistake 4: Overlooking Policy Coordination

Celebrities often hold multiple overlapping policies—general disability, specific body part, and production insurance. Without coordination, companies dispute responsibility, delaying payouts.

Fix: Use a single insurance broker managing all policies. Create clear primary/secondary designations.

Expert Tips for Celebrity Body Part Insurance

After consulting with Exceptional Risk Advisors and reviewing Lloyd’s of London underwriting guidelines, here are insider strategies.

Tip 1: Bundle with General Disability

Standalone body part policies cost 40% more than riders on comprehensive disability coverage. Bruce Springsteen reportedly saves $200,000 annually by bundling his voice coverage with general musician disability.

Expected Result: 25-35% premium reduction with identical coverage limits.

Tip 2: Negotiate “Aggravation” Clauses

Standard policies exclude pre-existing conditions. Smart negotiators include aggravation riders covering new injuries to previously hurt body parts. Kobe Bryant’s knee coverage included this after his 2003 surgery.

Expected Result: Coverage for 70% of reinjury scenarios normally excluded.

Tip 3: Include “Loss of Likeness” Provisions

Modern policies should cover digital replication rights. If a facial injury prevents CGI body double usage in films, celebrities lose residual income. Newer contracts address this emerging risk.

Expected Result: Protection for streaming-era revenue streams traditional policies ignore.

Tip 4: Maintain International Coverage

Celebrity careers span continents. Policies must cover medical treatment anywhere and pay in multiple currencies. Beyoncé’s world tour coverage includes 45 countries with local legal compliance.

Expected Result: No jurisdictional gaps canceling coverage during international performances.

Real Example: The $1 Billion Legs Case Study

Let’s examine Jennifer Lopez’s famous body part insurance in detail. This isn’t urban legend—it’s documented risk management.

The Asset: Lopez’s legs generate approximately $25 million annually through:

-

Fashion endorsements (Versace, Guess)

-

Fragrance campaigns requiring full-body imagery

-

Film roles emphasizing physical performance

-

Las Vegas residency choreography

The Risk: At age 54 (in 2026), Lopez faces increased injury probability from decades of dance training and high-heeled performances. A torn Achilles tendon could end her movement-heavy brand identity.

The Policy: Lloyd’s of London structured a $1 billion “umbrella” policy covering:

-

Direct leg injuries: $100 million

-

Career termination from mobility loss: $500 million

-

Brand value depreciation: $400 million

The Premium: Estimated $3-5 million annually (0.3-0.5% of coverage).

The Outcome: Lopez performed 100+ shows in her 2024-2025 residency without major incident. The policy’s psychological benefit arguably prevented the caution that ages performers prematurely.

Frequently Asked Questions

What is celebrity body part insurance?

Celebrity body part insurance is specialized disability coverage protecting income loss when a specific body part essential to a performer's career becomes damaged or nonfunctional. Unlike health insurance covering medical costs, these policies compensate for lost earning potential and career termination. Lloyd's of London pioneered this coverage in the 1940s for Hollywood stars, and it now protects $2 billion in celebrity assets globally. Policies typically cost 1-5% of coverage value annually and include provisions for total disability, partial impairment, and disfigurement affecting marketability.

How do celebrities get their body parts insured?

Celebrities work with specialized insurance brokers like Exceptional Risk Advisors or directly with Lloyd's of London underwriters. The process involves asset valuation (calculating the body part's income contribution), medical examination, and risk assessment of occupational hazards. Underwriters analyze endorsement contracts, performance schedules, and medical history before quoting premiums. High-value policies ($10M+) often require multiple insurers sharing risk through syndicates. The entire process takes 4-12 weeks and demands extensive documentation of the body part's economic role.

Why do celebrities insure their body parts instead of just having health insurance?

How much does celebrity body part insurance cost?

Premiums range from $10,000 annually for niche performers to $5 million for global superstars. Standard pricing follows 1-5% of coverage value: $1 million coverage: $10,000-$50,000/year $10 million coverage: $100,000-$500,000/year $100 million coverage: $1M-$5M/year Deductibles (out-of-pocket before payout) run $50,000-$500,000. Factors increasing costs include age, previous injuries, dangerous performance elements, and short career windows. Jennifer Lopez's $1 billion leg policy likely costs $3-5 million annually, while a classical pianist's $2 million hand coverage might cost just $20,000.

Is celebrity body part insurance worth it?

For A-list performers, absolutely. The math is simple: If a $30 million policy costs $300,000 annually and protects against a 5% annual career-ending risk, the expected value favors insurance ($1.5M expected loss vs. $300K premium). Beyond math, these policies provide contract security—promoters book insured stars confidently—and psychological freedom reducing performance anxiety. However, for B-list celebrities, the cost often exceeds realistic income protection needs. The coverage becomes worthwhile when annual premiums fall below 10% of protected income.

What are alternatives to celebrity body part insurance?

Alternatives include: General disability insurance: Covers any injury preventing work, but pays less for specific body part loss Production insurance: Film/TV policies covering cast injuries during specific projects Self-insurance: High-net-worth celebrities maintaining liquid reserves equal to policy values Contractual indemnification: Requiring studios/venues to assume injury liability Captive insurance companies: Celebrities forming personal insurers for tax advantages Most stars use hybrid approaches—general disability for baseline protection, body part policies for signature assets, and production insurance for specific projects.

How long does celebrity body part insurance coverage last?

Conclusion

Why do celebrities insure their body parts? Now you understand it’s not eccentricity—it’s sophisticated asset protection. From Jennifer Lopez’s billion-dollar legs to Julia Roberts’ million-dollar smile, these policies transform unpredictable physical risks into manageable business expenses.

The key lessons? Celebrity body part insurance protects income, not vanity. It requires specialized underwriting far beyond standard coverage. And when structured correctly, it provides psychological freedom that actually enhances performance longevity.

Ready to explore more entertainment industry risk management? Check out our

[Celebrity Financial Planning] pillar page for comprehensive guides on star wealth preservation.

What’s the most surprising celebrity insurance story you’ve heard? Drop it in the comments—I’d love to research whether it’s fact or urban legend!

Leave a Reply