Last Updated on March 29, 2026 by sarim50

How Celebrity Body Parts Insurance Actually Works (Sneaky Fine Print Exposed)

How Celebrity Body Parts Insurance Actually Works is a specialized risk management strategy that protects high-profile individuals against income loss when their money-making assets—legs, voices, smiles, or even hair—suffer damage. While headlines scream about

$1 billion legs and

$10 million smiles, the reality involves complex underwriting, sneaky exclusions, and a marketplace that dates back over 300 years.

I’ve analyzed dozens of these policies (and the fine print that comes with them). What I discovered? Most celebrity body part insurance isn’t what you think. Some policies are legitimate financial protection. Others? Clever PR stunts designed to grab headlines. Let’s pull back the curtain on this bizarre corner of the insurance world.

🔑 Key Takeaways

Lloyd’s of London underwrites 90% of celebrity body parts insurance through specialized syndicates

Premium costs range from $3,500/month for $1 million coverage to $500,000 for $200 million policies

Sneaky exclusions often void claims for pre-existing conditions, self-inflicted injuries, or “acts of God”

PR vs. Reality: Many “insurance announcements” are marketing stunts with murky policy details

Real coverage protects against loss of earnings, not just physical damage to the body part

What You’ll Learn

The exact mechanics of how celebrity body parts insurance actually works

Why Lloyd’s of London dominates this niche market

The shocking difference between PR stunt policies and real coverage

Sneaky fine print that could void a $40 million claim

Real examples: From Troy Polamalu’s $1 million hair to Cristiano Ronaldo’s €750 million left foot

How much these policies actually cost (and who pays)

Whether you can insure your own body parts (spoiler: yes, but it won’t be cheap)

What Is How Celebrity Body Parts Insurance Actually Works?

How Celebrity Body Parts Insurance Actually Works is a specialized form of disability insurance that compensates high-profile individuals for lost income if a specific body part essential to their career becomes damaged, scarred, or non-functional. Unlike standard health insurance that covers medical bills, these policies protect earning potential.

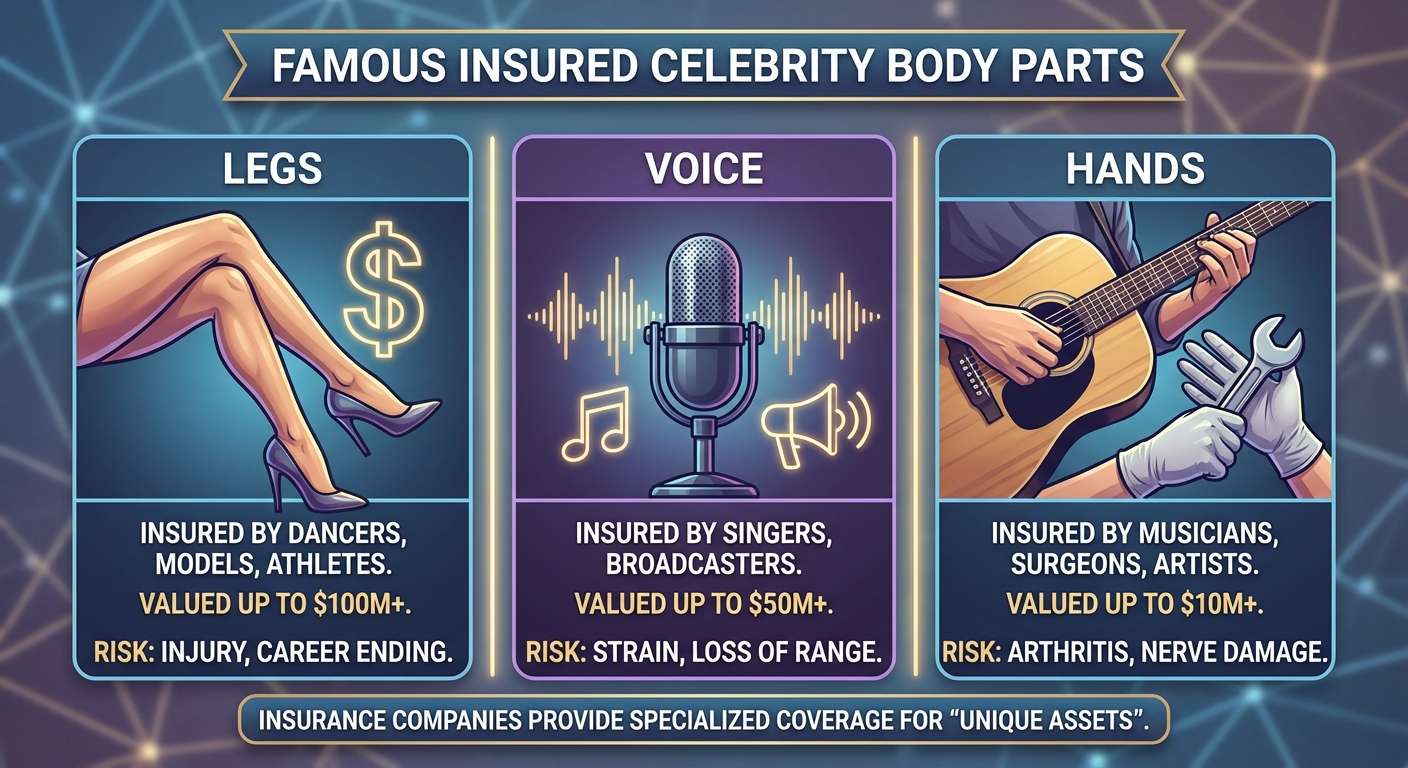

According to industry experts, this insurance functions as “loss of earnings” coverage rather than simple property protection. When Mariah Carey insured her vocal cords and legs for $70 million combined, she wasn’t protecting the physical assets—she was protecting her ability to tour, record, and perform.

The policies are typically underwritten by Lloyd’s of London, a 300-year-old insurance marketplace where specialized syndicates pool risk. Unlike traditional insurers, Lloyd’s operates as a subscription-based market where multiple financial backers share exposure.

How Celebrity Body Parts Insurance Actually Works: The Process

Step 1: Risk Assessment and Valuation

Before issuing a policy, underwriters conduct extensive medical examinations and career earning analyses. When Heidi Klum had her legs insured for £1.1 million ($2.2 million), she visited a London facility where specialists examined every inch of her limbs. “They would look at them, and I had one scar here from when I fell on a glass, so this [left leg] isn’t as pricey as this [right] one,” Klum explained.

The valuation process considers:

Current and projected earnings over the policy term

Career dependency on the specific body part

Medical history and existing conditions

Lifestyle factors (risky hobbies, travel schedules)

Step 2: Policy Structure and Coverage Terms

Most celebrity body parts insurance policies include:

| Coverage Component | Description | Example |

|---|

| Loss of Earnings | Compensation for canceled contracts/tours | Mariah Carey’s $35 million vocal cord policy |

| Medical Expenses | Treatment costs for injury recovery | Surgery and rehabilitation for damaged legs |

| Career Ending | Lump sum if career permanently ends | Cristiano Ronaldo’s €103 million leg coverage |

| Temporary Disability | Income replacement during recovery | 6-month payout for broken leg during film shoot |

Step 3: Premium Calculation

Premium costs vary dramatically based on risk. Oliver Lewis, the world’s fastest violinist, pays $3,500 monthly for $1 million hand coverage.

When Will Smith insured his 2018 Grand Canyon bungee jump, he paid $500,000 in premiums for $200 million in coverage.

The general rule: Premiums range from 0.25% to 2% of the insured value annually, though high-risk activities or pre-existing conditions can push rates higher.

Step 4: Claims Process and Payout

When a claim is filed, insurers investigate whether the injury falls within policy terms. Lloyd’s of London maintains a reputation for paying valid claims promptly—they paid out the Titanic’s £1 million hull coverage within 30 days of the 1912 sinking.

However, the sneaky fine print often includes:

Self-inflicted injury exclusions (voids claims for reckless behavior)

Pre-existing condition clauses (no coverage for prior injuries)

Specific activity limitations (coverage only applies during professional work)

Maintenance requirements (regular medical check-ups mandatory)

Celebrity Body Parts Insurance | Hilarious Guide for Normal People – AIOU Studio

Why Does How Celebrity Body Parts Insurance Actually Work Matter for Celebrities?

For A-list performers and athletes, specific body parts represent irreplaceable revenue generators. Cristiano Ronaldo’s left foot alone generates hundreds of millions in salary, endorsements, and image rights. When Real Madrid insured his legs for €103 million, they weren’t being dramatic—they were protecting a business asset.

Consider the economics: A singer like Bruce Springsteen earns $3-5 million per concert. If vocal cord damage cancels a 20-date tour, that’s $60-100 million in lost revenue. His $6 million voice insurance policy suddenly looks like smart business.

The same logic applies to:

Athletes whose legs or hands are essential to performance

Models whose faces or limbs are their brand

Chefs whose taste buds determine their Michelin stars

Surgeons whose hands perform life-saving procedures

What Happens If You Ignore How Celebrity Body Parts Insurance Actually Works?

Without proper coverage, a single injury can devastate a career. When Holly Madison prepared for her 2011 Las Vegas “Peepshow” revue, she recognized the risk: “If anything happened to my boobs, I’d be out for a few months and I’d probably be out a million dollars.” Her $1 million breast insurance policy with Lloyd’s of London provided financial security during the topless performance run.

The consequences of inadequate coverage include:

Bankruptcy: Lost income during recovery without compensation

Contract breaches: Inability to fulfill filming or tour obligations

Career termination: Permanent disability ending professional prospects

Legal liability: Lawsuits from studios or sponsors for unfulfilled commitments

How Much Does How Celebrity Body Parts Insurance Actually Work Cost?

Costs vary based on coverage amount, risk factors, and policy terms. Here’s what celebrities actually pay:

| Celebrity | Body Part | Coverage Amount | Estimated Annual Premium |

|---|

| Troy Polamalu | Hair | $1 million | ~$25,000-$50,000 |

| America Ferrera | Smile | $10 million | ~$250,000-$500,000 |

| Mariah Carey | Voice + Legs | $70 million | ~$1.75-$3.5 million |

| David Beckham | Legs | $195 million | ~$4.8-$9.75 million |

| Cristiano Ronaldo | Legs | €103 million (~$112M) | ~$2.8-$5.6 million |

Nick Cannon’s 2024 $10 million testicle insurance policy with Dr. Squatch represents a newer trend: brands paying premiums to protect their spokespersons’ assets. “I had to insure my most valuable assets,” Cannon stated, noting the policy was legitimate despite the publicity surrounding it.

The Sneaky Fine Print: What Insurers Don’t Advertise

Here’s where how celebrity body parts insurance actually works gets complicated. Many policies contain exclusions that could void claims when celebrities need them most.

Exclusion 1: Pre-Existing Conditions

If Jennifer Lopez had actually insured her famous curves (she denies the $27-300 million rumors), any prior cosmetic procedures or injuries could void claims. Insurers require full medical disclosure, and undisclosed history gives them grounds to deny payouts.

Exclusion 2: Self-Inflicted Injuries

When Taylor Swift joked about her cat scratching her “$40 million legs,” she highlighted a real issue: self-inflicted or pet-caused injuries often aren’t covered. Swift denied actually having the policy, but her Instagram post—”NOW YOU OWE ME 40 MILLION DOLLARS”—showed awareness of how these policies work.

Exclusion 3: Maintenance Requirements

Some policies require insured individuals to follow strict maintenance protocols. The Cadbury chocolate taster who insured her taste buds for £1 million in 2016 was barred from eating spicy foods or sword-swallowing—activities that could damage her insured asset.

Exclusion 4: “Acts of God” and War

Standard exclusions often include natural disasters, war, or terrorism. For celebrities touring globally, this creates significant coverage gaps.

Real Examples: Celebrity Body Parts Insurance Cases

Case Study 1: Troy Polamalu’s $1 Million Hair

In 2010, Head & Shoulders took out a $1 million policy on Troy Polamalu’s legendary Samoan hair. Jonathan Thomas of Watkins Syndicate at Lloyd’s of London stated: “We recognize that Troy Polamalu’s famed head of hair is truly legendary, and we are proud to partner with Head & Shoulders to protect it”.

The Fine Print Reality: This policy was primarily a PR stunt. The actual payout conditions remain murky—would hair loss from natural balding be covered? What about a bad haircut? The lack of disclosed details suggests marketing over serious risk management.

Case Study 2: Gordon Ramsay’s $10 Million Tongue

Gordon Ramsay reportedly insured his taste buds with Lloyd’s of London for $10 million. As a Michelin-star chef, his ability to taste and critique food directly impacts his television shows and restaurants.

Coverage Scope: The policy likely covers injury or disease affecting taste function, but probably excludes age-related taste decline or damage from Ramsay’s own notoriously spicy food challenges.

Case Study 3: David Beckham’s $195 Million Legs

David Beckham’s leg insurance represents one of the largest confirmed policies in sports history. The coverage was so substantial it required multiple insurance companies to share the risk.

Why It Worked: Unlike PR-driven policies, this was legitimate loss-of-earnings protection. Beckham’s legs generated income through:

Football contracts ($50+ million annually at peak)

Endorsements (Adidas, Pepsi, H&M)

Image rights and licensing

An injury ending his career would have cost hundreds of millions in future earnings.

Common Mistakes with How Celebrity Body Parts Insurance Actually Works

Mistake 1: Confusing PR Stunts with Real Coverage

Many “celebrity insures body part” headlines are marketing campaigns, not legitimate risk management. When Tom Jones was rumored to have $7 million chest hair insurance, he debunked it: “I’d shave my own bloody chest hair off for seven million dollars”.

The Fix: Verify policies through Lloyd’s of London confirmations or official insurance documents, not tabloid sources.

Mistake 2: Underestimating Exclusions

Celebrities often assume coverage is comprehensive when policies contain specific limitations. Michael Flatley of “Riverdance” fame once insured his legs for £40 million but later noted: “Not anymore. It’s a very different sum, but it’s very hard to get anyone to insure these legs”.

Age and prior injuries made coverage prohibitively expensive.

The Fix: Review exclusion clauses with specialized entertainment insurance attorneys before signing.

Mistake 3: Overvaluing Assets

Mariah Carey’s rumored $1 billion leg insurance from 2006 was tabloid fiction. Realistic valuations based on actual earning potential prevent premium waste and claim disputes.

The Fix: Use forensic accountants to determine precise loss-of-earnings values, not emotional attachment to body parts.

Expert Tips for How Celebrity Body Parts Insurance Actually Works

Tip 1: Work with Lloyd’s of London Coverholders

Specialized brokers accessing Lloyd’s syndicates provide the best coverage options. These professionals understand entertainment industry risks and can structure policies that actually pay out when needed.

Tip 2: Separate PR from Protection

If you’re insuring for publicity, be transparent. If you’re insuring for protection, prioritize coverage terms over headline value. The most valuable policies are the ones that pay when disaster strikes.

Tip 3: Maintain Meticulous Records

Successful claims require documentation of:

Pre-policy medical examinations

Income history proving earning potential

Incident reports and medical treatment records

Compliance with policy maintenance requirements

Tip 4: Consider “Key Person” Alternatives

For brands insuring celebrity assets, “key person” insurance sometimes offers better protection than body-specific policies. This covers loss of earnings if the celebrity becomes unable to perform, regardless of which body part fails.

How Celebrity Body Parts Insurance Actually Works vs. Standard Disability Insurance

| Feature | Body Parts Insurance | Standard Disability Insurance |

|---|

| Coverage Scope | Specific body part only | General inability to work |

| Payout Structure | Based on part’s earning contribution | Based on total income |

| Medical Requirements | Extensive examination of insured part | General health screening |

| Premium Cost | 0.25%-2% of insured value | 1%-3% of annual income |

| Claim Complexity | High (must prove part-specific impact) | Moderate |

| Best For | Assets generating specific income | General income protection |

Can Regular People Get Body Parts Insurance?

Yes, but it’s expensive and specialized. Surgeons, musicians, chefs, and other professionals whose livelihoods depend on specific body parts can purchase similar coverage through specialized brokers. However, without celebrity-level earnings, the cost-benefit ratio rarely makes sense for coverage exceeding $1-2 million.

For most professionals, standard disability insurance provides adequate protection at lower cost. Body parts insurance becomes viable when:

A specific body part generates 50%+ of income

The profession has high injury risk

Standard disability policies exclude occupation-specific risks

Frequently Asked Questions

What is How Celebrity Body Parts Insurance Actually Works?

How Celebrity Body Parts Insurance Actually Works is a specialized disability insurance that compensates high-profile individuals for income loss when career-essential body parts suffer damage. Unlike health insurance covering medical bills, these policies protect earning potential through Lloyd's of London syndicates, with coverage amounts ranging from $1 million to over $100 million depending on the asset's revenue generation

How do you get How Celebrity Body Parts Insurance Actually Works?

The process involves specialized brokers accessing Lloyd's of London markets, extensive medical examinations of the insured body part, forensic accounting to determine earning potential, and policy structuring with specific exclusions and maintenance requirements. Premiums typically cost 0.25% to 2% of the insured value annually

Why is How Celebrity Body Parts Insurance Actually Works important?

For celebrities and athletes, specific body parts generate millions in income through performances, endorsements, and appearances. Damage to these assets can trigger contract breaches, tour cancellations, and career termination. Insurance provides financial security during recovery or compensates for permanent disability

How much does How Celebrity Body Parts Insurance Actually Works cost?

Costs vary by coverage amount and risk factors. Oliver Lewis pays $3,500 monthly for $1 million hand coverage. Will Smith paid $500,000 in premiums for $200 million bungee jump coverage. Most celebrity policies range from $25,000 annually for $1 million coverage to $10 million annually for $195 million coverage .

Is How Celebrity Body Parts Insurance Actually Works worth it?

What are alternatives to How Celebrity Body Parts Insurance Actually Works?

How long does How Celebrity Body Parts Insurance Actually Works coverage last?

Policy terms typically range from 1-5 years for specific projects (films, tours) or 10-20 years for career-long coverage. Some policies include renewal options, though premiums increase with age and any injury history. Michael Flatley discovered that prior claims made his legs increasingly expensive to insure as he aged

What does How Celebrity Body Parts Insurance Actually Works cover?

Coverage includes loss of earnings from canceled contracts, medical expenses for injury treatment, lump-sum payments for career-ending disabilities, and temporary income replacement during recovery. However, policies contain extensive exclusions for pre-existing conditions, self-inflicted injuries, and activities outside professional scope .

Conclusion

Now you understand how celebrity body parts insurance actually works—and it’s far more complex than headlines suggest. While $1 billion legs make great tabloid fodder, the reality involves sophisticated underwriting through Lloyd’s of London, eye-watering premiums, and sneaky fine print that could void claims when celebrities need them most.

The key takeaway? Not all celebrity body part insurance is created equal. Some policies, like David Beckham’s $195 million leg coverage or Mariah Carey’s $70 million voice and leg protection, represent legitimate risk management protecting hundreds of millions in future earnings. Others, like rumored policies for Jennifer Lopez’s curves or Tom Jones’s chest hair, blur the line between financial protection and clever marketing.

If you’re considering body parts insurance (or just fascinated by this bizarre corner of the insurance world), remember: the most valuable policy is the one that actually pays when disaster strikes. That requires understanding the exclusions, maintaining meticulous records, and working with specialized brokers who access Lloyd’s of London markets.

What do you think—would you insure your body parts if you could afford it? Drop a comment below with which body part you’d protect and why!

Ready to dive deeper into celebrity risk management? Check out our comprehensive guide on

what is celebrity body parts insurance for the foundational concepts behind these fascinating policies.

Dark Side Celebrity Body Insurance Exposed | Fake Policies Revealed - aioustudio9edu

[…] in the comments and expose other fake policies you’ve encountered! Recommended next read: [How Does Celebrity Body Parts Insurance Work] | [Celebrity Financial Myths Debunked] body insurance fraudcelebrity body insurance […]